Taxes—just hearing the word can induce anxiety, right? Whether you’re a business owner or an individual trying to navigate the tax system, the complexity can feel overwhelming. And while the ultra-wealthy seem to have all the tax loopholes figured out, most people are left wondering if there are any legal strategies they can use to avoid paying more than necessary.

In this article, we’re going to dive into practical, legal ways to reduce your tax liability and keep more of your hard-earned money.

1. The Tax System: Feeling Stuck?

The tax code is complicated, and it often feels like it’s designed to benefit those who can afford top-tier accountants and advisors. But don’t worry—you don’t need an army of tax attorneys to pay less in taxes. You just need the right strategies.

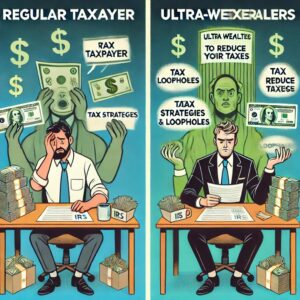

Visual Comparison – Taxpayer vs. Wealthy

This visual compares a regular taxpayer who is stressed and overwhelmed with writing checks to the IRS, while wealthy individuals are using tax strategies and loopholes to save on taxes.

With these tax-saving tips, you’ll discover how you can cut down on unnecessary tax payments legally.

2. Commuter Benefits: Tax-Free Savings on Transportation

If your workplace offers commuter benefits, you could be saving up to $300 a month on transportation costs tax-free. This includes costs related to:

- Buses and trains

- Ride-sharing services like Uber and Lyft

- Parking meters and garages

Commuter Benefits vs. No Tax Savings

This bar chart compares the potential annual savings ($3,600) from using commuter benefits versus not receiving tax savings for transportation costs.

3. Retirement Plans: Your Future and Tax Savings

Retirement accounts like 401(k)s or 403(b)s are not only essential for your future—they can significantly reduce your taxable income.

For 2023, you can contribute up to $22,500 into a 401(k), which directly lowers your taxable income. That means immediate savings in the short term and security for your future.

4. Health Savings Account (HSA): A Triple Tax Advantage

For those with high-deductible health plans, an HSA (Health Savings Account) offers a triple tax benefit:

- Contributions reduce your taxable income.

- Withdrawals for qualified health expenses are tax-free.

- Any earnings or interest in the account grow tax-free.

Triple Advantage of HSA

This graphic illustrates the triple tax advantage of an HSA, highlighting how contributions reduce income, withdrawals for health are tax-free, and the growth of the account is tax-free.

5. Flexible Spending Account (FSA): Use It or Lose It

If your employer offers an FSA, you can use pre-tax dollars for qualified medical expenses. However, FSAs operate on a “use it or lose it” basis—any unspent money at the end of the year is forfeited. Make sure you plan your healthcare spending carefully.

6. Dependent Care FSA: Save on Childcare

The Dependent Care FSA lets you pay for childcare with pre-tax money. This covers daycare, after-school programs, and even care for adult dependents. By using pre-tax dollars, you can potentially save thousands of dollars a year on these services.

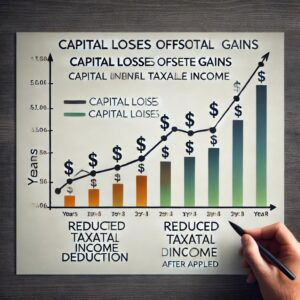

7. Capital Losses: Turning Losses into Tax Savings

Had a bad year with stocks or cryptocurrency? Capital losses can actually be a good thing when it comes to taxes. These losses can offset your taxable income, and if your losses exceed your gains, you can even carry them over to future years, further reducing your tax liability.

Capital Losses Reducing Taxable Income

This line graph shows how capital losses can offset gains and reduce taxable income over multiple years.

8. Long-Term Capital Gains: Lower Your Tax Rate

If you’ve had some wins in the stock market, make sure you hold those investments for at least a year. Long-term capital gains are taxed at much lower rates than short-term gains—sometimes as low as 0%, depending on your income level.

9. Review Your 1099-B Tax Form: Avoid Overpaying

One of the most common mistakes people make is failing to review their 1099-B tax form—the form that reports your stock transactions. If the form is missing the original price of a stock, the IRS might assume you paid $0, meaning you could be taxed on the full selling price.

Take a moment to review the details of your 1099-B and correct any discrepancies.

10. Margin Interest: Deductible Investment Expenses

If you trade on margin (borrowing money to invest), don’t forget that you can deduct margin interest from your taxable income. This is often overlooked because it’s not prominently listed on your tax forms.

11. Gambling Losses: Offset Your Winnings

Did you know that gambling losses can offset gambling winnings? If you spent time at the casino or betting on sports, you can use your losses to reduce your taxable winnings. Just make sure to keep accurate records!

12. IRA Contributions: Build for the Future, Save Today

Contributions to a Traditional IRA can reduce your taxable income, helping you save on taxes now while building a nest egg for the future.

13. 529 Plan: Tax-Free Education Savings

If you’re saving for education, a 529 plan offers significant benefits. While contributions aren’t deductible at the federal level, many states offer tax breaks. Plus, the growth is tax-free as long as the money is used for qualified educational expenses.

14. Fix Your W-4 Payroll Settings: Avoid Penalties

If you consistently owe money when you file your taxes, it might be time to adjust your W-4 payroll settings. Underpaying your taxes throughout the year can result in an underpayment penalty. Fixing your W-4 can save you from unexpected penalties and ensure you’re paying the right amount.

Wrap-Up: How the Ultra-Wealthy Keep Their Tax Bills Low

Finally, do you want to know how the top 50 billionaires in the world manage to keep their tax bills low? I’ve compiled their top strategies into one comprehensive guide. Click the link below to get your hands on it.

Tax Rates for Billionaires vs. Regular Taxpayers

This pie chart compares the average tax rates of billionaires (a smaller percentage) versus regular taxpayers (a larger percentage).

[Find Out Some Tax Tips from the World’s 50 Richest Billionaires]

Conclusion

The tax code may seem complicated, but with the right strategies, you can navigate it successfully—and legally. By making use of the tax breaks available to you, such as commuter benefits, retirement plans, HSAs, and more, you can significantly reduce your tax burden. And remember, planning is key. Make sure to review your forms carefully and always stay proactive when it comes to your finances.

If this article has helped you, make sure to share it with others and help spread these money-saving strategies!